The research team led by Prof. DUAN Maosheng of the Institute of Energy, Environment and Economy of Tsinghua University, has identified the potential double-counting risk when enterprises use consumption of renewable energy to achieve their Scope 2 emission reduction targets, and has quantitatively assessed the impact of double counting on the credibility of corporate emission reduction actions. Recently, the research findings were published online in Environmental Science & Technology with the title “Double Counting of Emission Reductions Undermines the Credibility of Corporate Mitigation Claims”

Abstract

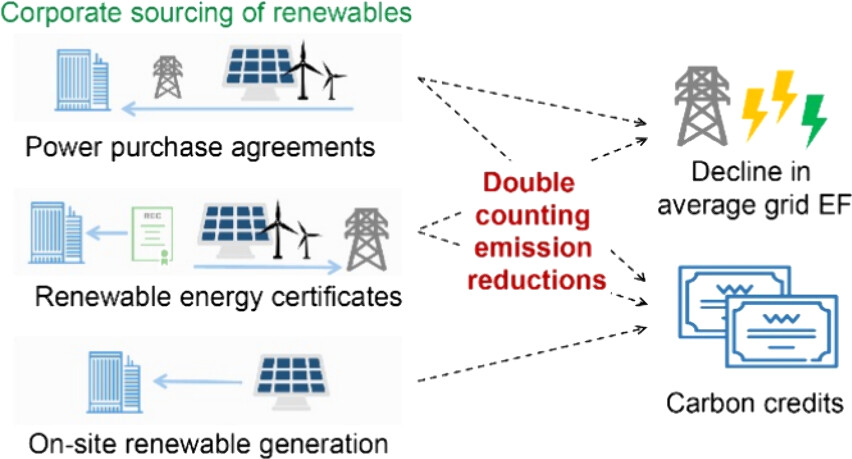

Companies are increasingly relying on emission reductions attributable to their adoption of renewable electricity to achieve net-zero emission targets. However, there is a risk of double counting of emission reductions threatening the credibility of corporate climate actions due to defective accounting rules of GHG emissions related to electricity consumption and the overlap between different market-based instruments, including carbon credit markets, renewable power purchase agreements, and renewable energy certificates. Using data of 63 major Chinese companies in seven sectors, we quantitatively assess the risks of double counting related to corporate sourcing of renewables and their consequent influences on the alignment of corporate emission trajectories with the 1.5 °C goal of the Paris Agreement. Results show that 7.1% of the electricity consumed by sample companies in 2021 was from renewable energy procurement and deployment, with which they reported 8.27 Mt of CO2e emission reductions compared to the scenario with no renewable electricity consumption. However, emission reductions that could be double counted are predicted to be 0.9–1.3 times as many as emission reductions that companies will report during 2021–2030. After adjustment of the reported emissions that might be underestimated due to double counting, the overall emission trajectories of sample companies are no longer aligned with the 1.5 °C goal. Our findings suggest that it is urgently needed to improve the corporate carbon accounting rules and increase the transparency of corporate carbon disclosures.

Link

https://pubs.acs.org/doi/10.1021/acs.est.4c03792